Choosing between a solar loan, lease, or PPA comes down to whether you want to own the system and how important upfront cost and long‑term savings are to you. A solar loan usually gives the best lifetime savings and boosts home value, but you’re responsible for maintenance and qualifying for financing. A solar lease or power purchase agreement (PPA) can reduce or eliminate upfront costs and keep things simple, but you won’t own the system and your savings are typically smaller over time. The right option depends on your credit, how long you’ll stay in the home, local electricity rates, and whether you’re comfortable taking on a loan.

Solar loan vs. lease vs. PPA is one of the most important decisions you’ll make when going solar. This guide is written for U.S. homeowners who want clear, no‑nonsense help choosing the right financing option. We’ll walk through how each works, what it really costs, and when each one makes sense (and when it doesn’t) so you can move forward with confidence.

Table of Contents

- Solar loans vs. leases vs. PPAs: the basics

- Key numbers: costs, savings, and payback

- Solar loans explained

- Solar leases explained

- Solar PPAs explained

- Side‑by‑side comparison: loan vs. lease vs. PPA

- State and utility considerations

- Which option is right for you?

- How to decide and what to do before getting quotes

- Frequently Asked Questions

- Summary

Solar loans vs. leases vs. PPAs: the basics

What each option really means

All three options help you avoid paying the full cost of a solar system upfront, but they work very differently:

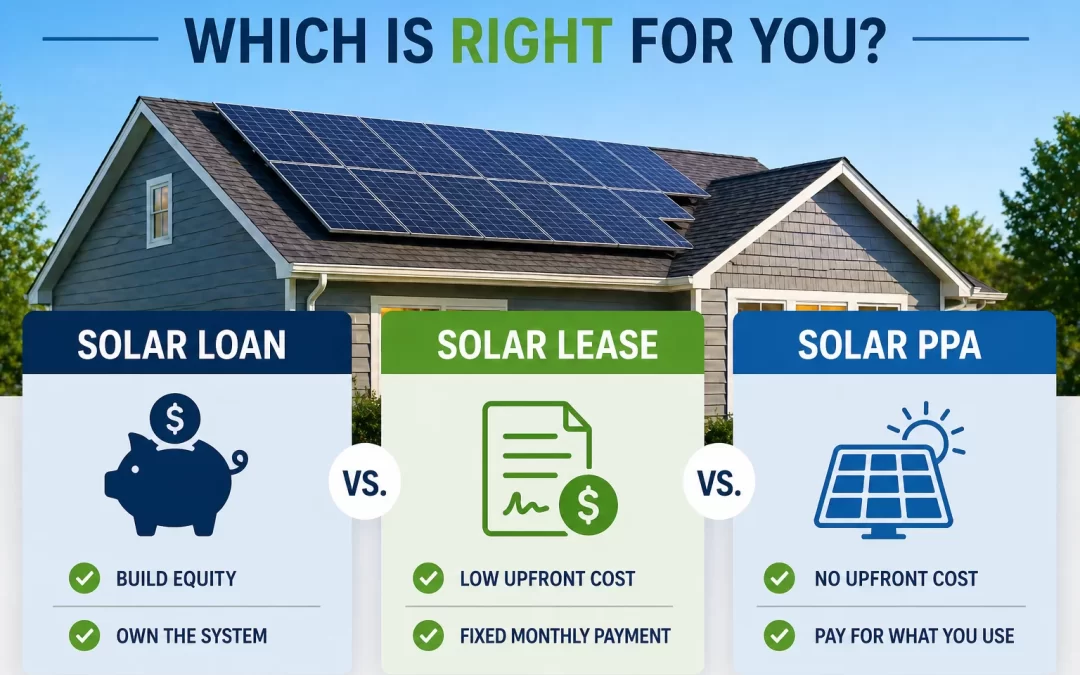

- Solar loan: You own the solar system. You borrow money to pay for it, then repay the loan over time (similar to a car loan or home improvement loan).

- Solar lease: A solar company or third party owns the system. You pay a fixed monthly fee to use the power it produces, usually for 20–25 years.

- Solar PPA (Power Purchase Agreement): A company owns the system and you pay for the electricity it generates, typically at a rate lower than your utility’s price per kWh.

All three can lower your electric bill. The main differences are ownership, who gets the tax incentives, and how much you save over time.

Who owns what — and why it matters

- With a loan, you own the panels, inverter, and other equipment.

- With a lease or PPA, the solar company owns the equipment and usually handles maintenance.

Ownership matters because it affects:

- Eligibility for incentives like the 30% federal tax credit (usually only available to the owner).

- Home value — owned systems can increase appraised value; leased/PPAs are more complicated.

- Long‑term savings — ownership usually wins over 20–25 years.

Key pros and cons at a glance

- Solar loan

- Pros: Best lifetime savings, you get incentives, increases home value, payment eventually ends.

- Cons: You take on debt, may need good credit, responsible for system issues (though warranties help).

- Solar lease

- Pros: Low or no upfront cost, simple, maintenance usually included.

- Cons: Smaller long‑term savings, no tax credit for you, can complicate selling your home.

- Solar PPA

- Pros: Low or no upfront cost, pay only for power produced, maintenance included.

- Cons: Rate escalators can eat into savings, no incentives for you, similar home‑sale issues as leases.

Key numbers: costs, savings, and payback

Typical system cost and size

For a typical U.S. home, here are realistic 2026 benchmarks:

- Average system size: 6–10 kW (about 15–25 panels).

- Cost per watt: $2.50–$3.50 before incentives.

- Total system cost: roughly $28,000–$32,000 before incentives.

- After the 30% federal tax credit, that drops to about $19,600–$22,400, if you qualify and can use the credit.

Actual costs depend on your roof, equipment quality, local labor rates, and system size. For a deeper breakdown by system size, see the average solar panel cost by system size guide.

Typical savings and payback

Nationally, homeowners who own their systems (cash or loan) often see:

- Average annual bill savings: about $1,300–$1,500.

- Payback period (time for savings to equal net cost): about 7–9 years.

- Panel lifespan: performance warranty of 25–30 years, with typical useful life of 30–35 years.

Leases and PPAs usually have shorter payback in the sense of “instant savings” (you may save in year one with no upfront cost), but lower total savings over 20–25 years because you never stop paying.

What affects these numbers most

- Your utility rate and how fast it’s rising.

- Net metering or other credit programs from your utility.

- Roof orientation and shading (how much power your system can produce).

- Local incentives and whether you or the solar company receives them.

- Loan terms (interest rate, length) or lease/PPA escalator rates.

Because these variables are so local, it’s smart to compare multiple quotes and have installers run the numbers for your exact home. Before you do that, it can help to confirm that solar makes financial sense in your situation using an honest overview like the is solar worth it guide.

Solar loans explained

How a solar loan works

A solar loan lets you spread the cost of your system over time while still owning it. Common structures include:

- Secured loans (like home equity loans or HELOCs): often lower interest rates but may use your home as collateral.

- Unsecured solar loans: no home collateral, but rates can be slightly higher.

- Term lengths: typically 10–25 years.

You’ll usually make a fixed monthly payment. In many cases, that payment plus your new, smaller electric bill is similar to or less than your old utility bill from day one.

Key numbers for solar loans

- Loan amount: often the full system cost (e.g., $28,000–$32,000).

- Net cost after tax credit: if you qualify for the 30% federal tax credit and apply it, your effective cost can drop to around $19,600–$22,400.

- Interest rates: commonly in the 3–8% APR range, depending on credit and loan type.

- Typical monthly payment: often $100–$250, depending on system size, loan term, and rate.

Many solar loans are structured assuming you’ll use your tax credit as a lump‑sum payment in year one. If you can’t use the full credit or choose not to apply it to the loan, your payment may be higher than the “teaser” payment shown in sales pitches. Always ask the lender to show you the payment with and without applying the tax credit.

What affects whether a solar loan is a good deal

- Your credit score and debt‑to‑income ratio (affects approval and interest rate).

- Loan term: longer terms lower the monthly payment but increase total interest paid.

- Electricity rates: higher rates usually mean better savings from going solar.

- How long you’ll stay in the home: the longer you stay, the more you benefit from owning.

When a solar loan works in your favor

- You want maximum long‑term savings and are comfortable with a loan.

- You expect to stay in your home at least 7–10 years.

- You can likely use the 30% federal tax credit (confirm with a tax professional).

- You like the idea of increasing your home’s value with an owned system.

When a solar loan may not be the best choice

- Your credit score is low or you already have a lot of debt.

- You’re planning to move in the next 3–5 years and are unsure how buyers in your area view solar.

- You’re uncomfortable taking on new monthly payments, even if your total energy costs may drop.

- You can’t realistically use the tax credit and the loan is structured assuming you will.

If any of these apply, a lease, PPA, or even waiting a few years might be more comfortable.

Solar leases explained

How a solar lease works

With a solar lease, a company installs and owns the system on your roof. You agree to pay a fixed monthly fee to use the power it generates, usually for 20–25 years.

Key features:

- Little or no upfront cost — many leases are $0 down.

- Fixed monthly payment that may include a small annual increase (escalator).

- Maintenance and repairs are typically the company’s responsibility.

- You usually have an option to buy the system at the end of the term or renew the lease.

Numbers to watch in a lease

- Starting monthly lease payment: often designed to be 10–30% lower than your current electric bill.

- Annual escalator: commonly 1–3% per year.

- Term length: usually 20–25 years.

- End‑of‑term options: buyout price, renewal terms, or system removal.

The company that owns the system typically claims the 30% federal tax credit and any other incentives, which is part of how they can offer low or no upfront cost.

When a solar lease works in your favor

- You want immediate bill savings with no or low upfront cost.

- You prefer a simple, hands‑off arrangement where someone else handles maintenance.

- Your credit or debt situation makes a loan less attractive.

- You’re okay with modest long‑term savings rather than maximizing every dollar.

When a solar lease can backfire

- Escalator rates are too high, and your lease payment eventually catches up to or exceeds what your utility bill would have been.

- You need to sell your home before the lease ends and the buyer doesn’t want to assume the lease.

- You later decide you’d rather own the system, but the buyout price is high.

- Your utility rates stay flat or rise slowly, reducing the value of your lease savings.

Always ask the leasing company to show you a worst‑case scenario (low utility inflation, lower system production) so you can see how sensitive your savings are to those assumptions.

Solar PPAs explained

How a solar PPA works

A solar power purchase agreement (PPA) is similar to a lease, but instead of paying a fixed monthly fee, you pay for the actual electricity the system produces, usually at a rate lower than your utility’s price per kilowatt‑hour (kWh).

Typical features:

- $0 or low upfront cost.

- You pay a per‑kWh rate (for example, $0.12/kWh) instead of a fixed lease payment.

- The rate may include an annual escalator (e.g., 1–3% per year).

- The company owns, monitors, and maintains the system.

Key PPA numbers

- Starting PPA rate: usually set below your current utility rate (for example, if your utility charges $0.18/kWh, the PPA might start at $0.13–$0.15/kWh).

- Escalator: often 1–3% annually.

- Contract length: typically 15–25 years.

- Production guarantees: minimum output the company promises, with bill credits if they fall short.

As with leases, the PPA provider usually keeps the tax credit and incentives.

When a PPA works in your favor

- You want no upfront cost and immediate savings.

- You like paying only for power actually produced, not a fixed lease payment.

- You want maintenance and performance risk on the solar company, not you.

- Your utility rates are high and likely to keep rising.

When a PPA may not be ideal

- The starting PPA rate isn’t much lower than your utility rate.

- The escalator is high, so in later years you may pay close to or more than utility prices.

- You plan to sell your home soon and aren’t sure how buyers will feel about assuming a PPA.

- Your roof has shading or orientation issues that limit production, reducing your savings.

As with leases, ask the provider to show you savings under conservative assumptions, not just best‑case projections.

Side‑by‑side comparison: loan vs. lease vs. PPA

Ownership, incentives, and savings

| Feature | Solar Loan | Solar Lease | Solar PPA |

|---|---|---|---|

| Who owns the system? | You | Solar company | Solar company |

| Upfront cost | Low to high (depends on down payment) | Usually low or $0 | Usually low or $0 |

| Monthly payment type | Fixed loan payment | Fixed lease payment (may escalate) | Per‑kWh rate (may escalate) |

| Who gets tax credit/incentives? | You (if eligible) | System owner | System owner |

| Maintenance responsibility | You (often covered by warranties) | Solar company | Solar company |

| Typical lifetime savings | Highest | Moderate | Moderate |

| Impact on home value | Usually positive | More complex; depends on buyer | More complex; depends on buyer |

Real‑world example (simplified)

Assume a 7 kW system costing $30,000 before incentives, producing about 10,000 kWh/year, and your utility rate is $0.18/kWh.

- Loan scenario

- Net cost after 30% tax credit: $21,000 (if you can use it).

- Loan: 15 years at 5% APR → about $166/month.

- Electric bill drops by roughly $150/month on average.

- In early years, your total (loan + small utility bill) might be similar to your old bill; after the loan is paid off, you keep most of the $1,300–$1,500/year savings.

- Lease scenario

- Lease payment: $120/month, 2% annual escalator.

- Utility bill drops by $150/month → net savings of about $30/month in year one.

- Over time, as the lease payment rises, your monthly savings may shrink unless utility rates rise faster.

- PPA scenario

- PPA rate: $0.13/kWh vs. $0.18/kWh utility rate.

- 10,000 kWh/year → about $1,300/year to PPA provider instead of $1,800 to utility → savings of about $500/year.

- If the PPA escalator is lower than your utility’s rate increases, your savings can grow; if not, they may flatten out.

These are simplified examples; actual numbers will vary, but they show why loans usually win on total savings while leases and PPAs win on simplicity and low upfront cost.

State and utility considerations

Why your location changes the answer

The best choice between a solar loan, lease, or PPA depends heavily on where you live. Key local factors include:

- Electricity prices and how fast they’re rising.

- Net metering or similar programs that credit you for extra solar power sent to the grid.

- State and local incentives (rebates, tax credits, performance payments).

- Whether leases and PPAs are even allowed — some states restrict them.

To see how your state stacks up on costs and savings, check the solar cost by state guide.

Net metering and your financing choice

Net metering is a policy where your utility credits you for extra solar power you send to the grid, often at or near the retail rate. This can significantly improve the economics of owning a system (cash or loan).

- In states with strong net metering, ownership via a loan often provides excellent payback.

- In states where net metering has been reduced or replaced with lower export rates, leases and PPAs may structure their offers to still provide savings, but you’ll want to look closely at the assumptions.

If you’re not familiar with net metering, our overview of what net metering is and how much it can save is a helpful starting point.

When local incentives favor one option

- If your state offers generous rebates or tax credits that you can use, owning with a loan usually makes the most sense.

- If you can’t use tax credits (for example, low taxable income), a lease or PPA provider might be able to monetize those incentives and pass some value to you through lower rates.

- Some utilities offer special programs that pair better with ownership than with third‑party systems.

Because incentive rules change, it’s wise to confirm current programs with a local installer and, for tax‑related questions, a qualified tax professional.

Which option is right for you?

Solar loan is usually best if you:

- Have good credit and can qualify for a reasonable interest rate.

- Plan to stay in your home at least 7–10 years.

- Can likely use the 30% federal tax credit and any state incentives.

- Want to maximize long‑term savings and increase home value.

- Are comfortable taking on a loan in exchange for lower energy costs.

Solar lease may be best if you:

- Want no or very low upfront cost.

- Prefer a simple, predictable monthly payment.

- Don’t want to worry about maintenance or repairs.

- Are okay with moderate savings instead of squeezing out every dollar.

- Have limited ability to use tax credits or don’t want to deal with them.

Solar PPA may be best if you:

- Like the idea of paying only for power actually produced.

- Want $0 down and immediate savings.

- Live in an area with high electricity rates and good solar production.

- Prefer the solar company to handle performance risk and maintenance.

When waiting or not going solar is the right call

- Your roof needs major repairs or replacement soon.

- Your roof has heavy shading or poor orientation that limits production.

- You plan to move within a few years and don’t want to deal with transferring a loan, lease, or PPA.

- Your utility rates are very low, and local incentives are minimal.

In these cases, it may be better to address roof issues first, consider community solar, or simply wait until conditions improve.

How to decide and what to do before getting quotes

Step 1: Gather your basic information

Before talking to installers or finance providers, have these handy:

- 12 months of electric bills (kWh usage and total cost).

- Your roof age and condition (and any known issues).

- How long you expect to stay in the home.

- A rough idea of your credit score range.

Step 2: Decide your priorities

Rank what matters most to you:

- Lowest upfront cost vs. highest long‑term savings.

- Owning the system vs. keeping it off your balance sheet.

- Simple, hands‑off vs. maximum financial benefit.

Your answers will naturally point you toward a loan, lease, or PPA.

Step 3: Get multiple quotes — and compare apples to apples

It’s wise to get at least 2–3 quotes from reputable installers and finance providers. When you do, compare:

- Total system size (kW) and estimated annual production (kWh).

- All‑in cost before and after incentives (for loans).

- Monthly payment and escalator (for leases and PPAs).

- Assumed utility rate increases in their savings projections.

- Warranties on equipment, workmanship, and production.

Understanding the equipment in your quote also helps you compare offers more accurately; the solar panels and equipment guide can help you decode model numbers and specs.

Questions to ask every installer or finance provider

- “Is this a loan, lease, or PPA? Who will own the system?”

- “Who gets the 30% federal tax credit and any state incentives?”

- “What interest rate or escalator are you using, and for how long?”

- “What happens if I sell my home before the contract ends?”

- “What are my maintenance and repair responsibilities?”

- “Can you show me a conservative savings scenario, not just best case?”

For any tax‑related questions, always confirm details with a qualified tax professional; installers can explain how programs generally work but cannot give personalized tax advice.

Frequently Asked Questions

Is a solar loan better than a lease or PPA?

A solar loan is usually better if you want to maximize long‑term savings and are comfortable owning the system and taking on a loan. Leases and PPAs are better if you want little or no upfront cost and a simple, hands‑off arrangement, but they typically provide smaller total savings over 20–25 years.

Who gets the 30% federal tax credit with a solar lease or PPA?

With a solar lease or PPA, the company that owns the system usually claims the 30% federal tax credit and any other incentives. They may pass some of that value to you through lower monthly payments or kWh rates, but you generally cannot claim the credit yourself.

Can I sell my house if I have a solar lease or PPA?

Yes, but the buyer typically must either assume the lease/PPA or you must pay it off or buy out the system at closing. This can be smooth if the contract terms are attractive, but it can also slow down a sale if buyers are hesitant, so it’s important to understand transfer and buyout options before signing.

What credit score do I need for a solar loan?

Many solar lenders look for credit scores in the mid‑600s or higher, with the best rates usually going to borrowers in the 700s and above. Requirements vary by lender, so if your credit is borderline, it’s worth getting quotes from multiple providers or considering a lease or PPA.

Do solar panels still save money if I finance them?

In many cases, yes — even with a loan, your combined loan payment and smaller electric bill can be similar to or lower than your old utility bill, and once the loan is paid off, your savings typically grow significantly. The exact outcome depends on your loan terms, local electricity rates, and how much sun your roof gets.

How long do solar panels last compared to loan or lease terms?

Most solar panels come with 25–30 year performance warranties and often keep producing power for 30–35 years. Loan terms are usually 10–25 years, and leases/PPAs are commonly 20–25 years, so an owned system can keep saving you money for years after the financing ends.

Summary

- A solar loan usually offers the best lifetime savings and home value boost, especially if you can use the 30% federal tax credit and plan to stay put for several years.

- Leases and PPAs trade some long‑term savings for low or no upfront cost and a simple, hands‑off experience, but you won’t own the system or claim incentives.

- Key numbers to watch include system cost ($28,000–$32,000 before incentives), annual savings ($1,300–$1,500 on average), payback period (7–9 years for ownership), and any escalators in leases/PPAs.

- Your location, utility rates, roof, and time horizon in the home have a major impact on which option makes sense.

- The smartest next step is to get multiple quotes, compare loan vs. lease vs. PPA side by side, and confirm tax details with a professional before signing anything.

If you’re ready to see real numbers for your home, getting personalized quotes is the best way to compare a solar loan, lease, and PPA on equal footing. A few minutes now can clarify your options and show whether solar is worth it for your situation. When you’re ready, you can start by requesting tailored offers at /get-my-quote/ and reviewing them at your own pace.