Most solar lenders look for a credit score of around 650–700 or higher to approve traditional solar loans with good terms. Some programs will approve scores in the low 600s, but you may see higher interest rates or need a larger down payment. If your score is below 600, approval is possible but harder, and you may need a co-borrower or to consider alternatives like leases or community solar. Exact requirements vary by lender, state, and whether the loan is secured (tied to your home) or unsecured.

Financing solar can make going solar possible without paying everything upfront, but your credit score plays a big role in what you qualify for and what it will cost over time. This guide is for U.S. homeowners who want a clear, honest look at what credit score you need to finance solar, what happens if your score isn’t perfect, and what options you still have. The goal is to help you decide whether to move forward now, improve your credit first, or consider other ways to save on energy.

Table of Contents

- What Credit Score Do You Need to Finance Solar?

- How Different Solar Financing Options Treat Your Credit Score

- Real Numbers: Solar Costs, Savings, and How Credit Affects Them

- State and Utility Differences That Affect Solar Financing

- Can You Get Solar With Bad or Fair Credit?

- When Financing Solar Works in Your Favor

- When Financing Solar May Not Be a Good Idea

- How to Decide Your Next Step (And What to Do Before Getting Quotes)

- Frequently Asked Questions

- Summary: Key Takeaways on Credit Scores and Solar Financing

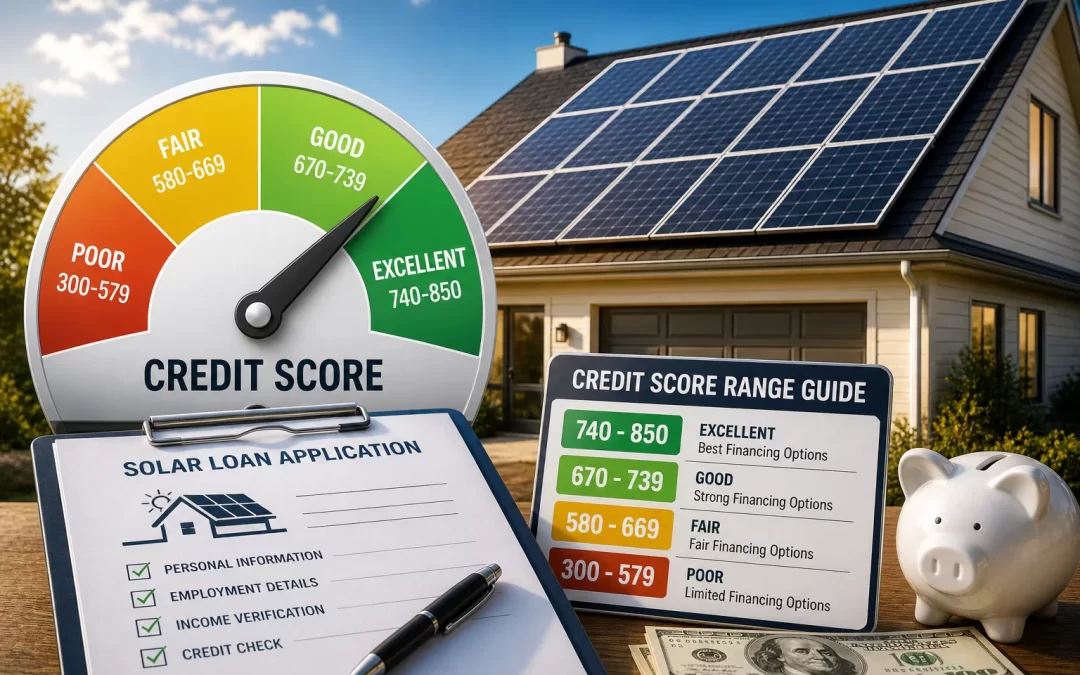

What Credit Score Do You Need to Finance Solar?

Typical credit score ranges for solar loans

Most residential solar loans are designed for “prime” borrowers, but there is a range:

- 700+: Usually qualifies for the best rates and terms with many lenders.

- 650–699: Often approved, but with slightly higher interest rates.

- 600–649: Approval is possible with some lenders, often at higher rates or with more conditions.

- Below 600: Traditional solar loans are harder to get; you may need a co-borrower or alternative options.

Each lender sets its own minimums, and some installer-partner programs may accept lower scores than a bank or credit union. Your income, debt-to-income ratio, and home equity can matter as much as your credit score.

Why lenders care about your credit score

Your credit score is a quick way for lenders to estimate how likely you are to repay a loan. For solar financing, they look at:

- Payment history: On-time vs. late payments on credit cards, auto loans, and mortgages.

- Credit utilization: How much of your available credit you’re using.

- Length of credit history: How long your accounts have been open.

- Recent credit inquiries: How many new accounts or applications you’ve had recently.

Even if your score is borderline, strong income and low existing debt can help you qualify. On the other hand, a good score with very high existing debt can still cause problems.

Minimum credit score vs. “good enough” score

There’s a difference between the minimum score to get approved and the score that gets you a loan that actually makes financial sense:

- Minimum approval score: Often around 600–650 for many solar loan programs.

- Better-value score: Around 680–700+ to access lower interest rates that keep your monthly payment competitive with your current electric bill.

If you barely meet the minimum, you may still be approved, but the interest cost over 10–25 years can eat into or even erase your solar savings.

How Different Solar Financing Options Treat Your Credit Score

1. Unsecured solar loans (most common)

Unsecured loans are not tied to your home as collateral. They’re common through solar installers and online lenders.

- Typical minimum credit score: 650–680, though some go lower.

- Loan terms: Often 10–25 years.

- Interest rates: Highly dependent on credit score; lower scores see higher rates.

Because the lender has more risk (no collateral), they rely heavily on your credit score and income. These loans are easy to apply for but can be expensive if your score is below the high 600s.

2. Secured loans (home equity loans, HELOCs, and property-backed solar loans)

Secured loans use your home or property as collateral, which can change the credit score requirements.

- Home equity loans / HELOCs: Many banks look for scores around 660–680+, plus enough equity in your home.

- Property-assessed clean energy (PACE) loans: Available in some states; approval is often based more on home equity and property tax history than just credit score.

Secured loans can offer lower interest rates than unsecured solar loans, but they come with a serious caveat: if you don’t pay, your home could be at risk. It’s important to discuss this with a financial professional before using home equity for solar.

3. Solar leases and power purchase agreements (PPAs)

With leases and PPAs, you don’t own the solar system; you pay a monthly fee or per-kilowatt-hour rate to use the power it produces.

- Typical minimum credit score: Often around 600–650, sometimes lower than for loans.

- Ownership: The solar company owns and maintains the system.

- Incentives: The company, not you, usually claims the federal tax credit and other incentives.

Leases and PPAs can be easier to qualify for if your credit is fair, but they usually offer less long-term financial benefit than owning your system outright.

4. Paying cash (no credit score needed)

If you pay for solar in cash, your credit score doesn’t matter at all for the purchase itself. However:

- You still need to consider your overall financial picture and emergency savings.

- Paying cash means you avoid interest entirely, which can significantly improve your long-term savings.

For homeowners with the savings available, cash is often the best financial option, but it’s not realistic for everyone.

Real Numbers: Solar Costs, Savings, and How Credit Affects Them

Typical cost of a home solar system

As of 2026, a typical residential solar system in the U.S. costs:

- Total system cost: About $28,000–$32,000 before incentives.

- After 30% federal tax credit: Roughly $19,600–$22,400, assuming you qualify for the full credit.

- Cost per watt: Around $2.50–$3.50 per watt installed.

- Average system size: 6–10 kW, or about 15–25 panels for a typical U.S. home.

These are national averages. Your actual cost depends on your roof, local labor rates, equipment choices, and state incentives. A reputable installer should provide a detailed, line-item quote.

Typical savings and payback period

On average, homeowners see:

- Annual electric bill savings: About $1,300–$1,500 per year.

- Payback period (if you buy and own the system): Around 7–9 years nationally.

- Panel lifespan: 25–30 years performance warranty, with many systems lasting 30–35 years.

Over 25–30 years, many homeowners save tens of thousands of dollars compared to staying fully on grid power, but this depends heavily on your local utility rates and solar production. Our 25-year solar vs. grid cost comparison guide walks through how those long-term numbers play out.

How your credit score changes the math

Your credit score doesn’t change how much sunlight hits your roof, but it does change how much you pay to finance your system:

- Higher credit score (700+): Lower interest rates mean more of your monthly payment goes toward the system itself, not interest.

- Mid-range score (650–699): You may still save money, but a higher interest rate can lengthen your payback period.

- Lower score (600–649): Interest costs can be high enough that your monthly loan payment is close to or even higher than your current electric bill.

In other words, two neighbors with identical roofs and systems can see very different financial outcomes if one has a 740 credit score and the other has a 620 score, simply because of financing costs.

Federal tax credit and your financing

The federal solar Investment Tax Credit (ITC) is 30% through at least 2032. This can significantly reduce your net cost, but:

- You must have enough tax liability to use the credit; it is not a refund check.

- Many solar loans are structured assuming you’ll apply the tax credit as a lump-sum payment in year one to keep your monthly payment lower.

Because tax situations are personal, it’s wise to confirm your eligibility with a tax professional. Our solar incentives and tax credits guide explains how the ITC generally works, but it is not a substitute for professional advice.

State and Utility Differences That Affect Solar Financing

Why your state matters

Your credit score is only one piece of the puzzle. Where you live can have just as much impact on whether solar financing makes sense:

- Electricity rates: Higher utility rates (often in states like California, New York, Massachusetts, and Hawaii) make solar savings larger.

- State incentives: Rebates, state tax credits, and performance payments can reduce your net cost.

- Net metering rules: These determine how you’re credited for excess solar power you send back to the grid.

In a strong solar state with high utility rates, even a slightly higher loan interest rate can still pencil out well. In a low-rate state with weak incentives, you may need very favorable financing terms to see a good return. To see how this plays out where you live, our state-by-state guide, Is Solar Worth It in Your State?, is a helpful starting point.

Utility policies and solar financing

Some utilities offer on-bill financing or special loan programs for energy upgrades, including solar. These can:

- Have more flexible credit requirements than traditional banks.

- Allow you to repay the loan on your utility bill, sometimes with favorable terms.

Availability varies widely by region. Ask your utility if they have any solar or energy-efficiency financing programs, and compare those terms to what solar installers and local lenders offer.

Can You Get Solar With Bad or Fair Credit?

If your credit score is below 650

Having a score under 650 doesn’t automatically rule out solar, but it does change your options:

- Approval is less certain: Some lenders will decline, while others may approve at higher rates.

- Monthly payment may be higher: Interest costs can push your payment above your current electric bill.

- More documentation: Lenders may ask for proof of income, employment, or additional financial details.

In this range, it’s especially important to run the numbers carefully and not just focus on “no money down” offers.

Strategies if your credit is fair or poor

If your credit isn’t where you want it to be, you still have options:

- Use a co-borrower: A spouse or family member with stronger credit can help you qualify for better terms.

- Improve your score first: Paying down credit card balances, catching up on late payments, and avoiding new debt for 6–12 months can sometimes raise your score enough to unlock better rates.

- Consider smaller projects: Starting with energy-efficiency upgrades (insulation, air sealing, efficient HVAC) may have lower financing requirements and can reduce your energy use before you size a solar system.

Alternatives if you can’t qualify for good solar financing

If you can’t get a solar loan with reasonable terms, it may be better to wait or consider alternatives:

- Solar leases or PPAs: Easier to qualify for, but you won’t own the system or claim the tax credit.

- Community solar: Lets you subscribe to a share of a larger solar farm and get bill credits, often with no credit check or a very soft one. Our guide to community solar explains how this works.

- Energy-efficiency improvements: Lower your bills now while you work on improving your credit for a future solar purchase.

It’s better to pass on a bad financing deal than to lock yourself into a long-term contract that doesn’t truly save you money.

When Financing Solar Works in Your Favor

Signs solar financing is likely a good move

Financing solar tends to work well when:

- Your credit score is solid: Around 680–700+ and your debt-to-income ratio is reasonable.

- Your electric bill is high: $120–$150+ per month or more, especially in high-rate states.

- You plan to stay in your home: At least 7–10 years to get through the typical payback period.

- Your roof is in good shape: No major repairs needed in the next 10–15 years.

In these situations, a well-structured solar loan can replace part of your utility bill with a predictable payment that eventually goes away, while your panels keep producing power.

How to tell if the numbers work for you

Before signing anything, look at:

- Monthly loan payment vs. current bill: Is your payment equal to or lower than what you pay now, or at least close with a clear long-term benefit?

- Total interest paid: Over the life of the loan, how much interest will you pay compared to your projected savings?

- Payback period: Does the payback (often 7–9 years) fit your plans for staying in the home?

Our solar payback period calculator can help you estimate when your system might pay for itself based on your specific numbers.

When Financing Solar May Not Be a Good Idea

Situations where solar financing can backfire

Even if you can qualify for a solar loan, it’s not always the right move. Be cautious if:

- Your credit score is low and the interest rate is high: A high rate can wipe out your savings.

- You plan to move soon: If you expect to sell your home in 3–5 years, you may not reach payback before moving.

- Your roof is shaded or small: Limited production means lower savings, which makes high-interest financing harder to justify.

- Your budget is already tight: Adding a long-term payment could create financial stress, especially if your income is uncertain.

In these cases, it may be smarter to wait, improve your credit, or explore other options to cut your energy costs. Our guide on when solar doesn’t make sense walks through these scenarios in more detail.

Red flags in solar financing offers

Regardless of your credit score, watch out for:

- Very long terms (25+ years) with high rates: You may pay far more in interest than you save on electricity.

- Complex “dealer fees” rolled into the loan: These can quietly add thousands to your cost.

- Pressure to sign quickly: A reputable installer will give you time to review and compare offers.

If something in the contract is unclear, ask the installer or lender to explain it in plain language. If they can’t or won’t, that’s a sign to step back.

How to Decide Your Next Step (And What to Do Before Getting Quotes)

Is now the right time for you to finance solar?

Ask yourself these questions:

- Is my credit score at least in the mid-600s, or do I have a co-borrower with stronger credit?

- Are my electric bills high enough that solar could realistically save me $1,300–$1,500 per year?

- Do I plan to stay in this home long enough to reach payback (7–9 years on average)?

- Is my roof in good condition and mostly unshaded?

If you can answer “yes” to most of these, it’s worth getting quotes and seeing real numbers for your home. If not, consider whether improving your credit or tackling lower-cost energy upgrades first makes more sense.

What to do before you request solar quotes

To get accurate, useful quotes, gather:

- 12 months of electric bills: Installers use this to size your system and estimate savings.

- Basic roof information: Age of your roof, material (asphalt shingle, tile, metal), and any known issues.

- Your credit snapshot: Know your approximate score and any major issues (recent late payments, high card balances).

It also helps to read a straightforward overview of solar basics first; our main guide, Is Solar Worth It?, explains how to think about solar as a long-term investment.

Questions to ask installers about financing

When you talk with installers or lenders, ask:

- What minimum credit score do you require for your main loan products?

- What is the interest rate, term length, and total estimated interest over the life of the loan?

- Does this loan assume I’ll use the 30% federal tax credit as a lump-sum payment? What happens if I can’t?

- Are there any dealer fees or prepayment penalties?

Getting clear answers to these questions will help you compare offers and avoid surprises later.

Why getting multiple quotes matters

Even with the same credit score, different installers and lenders can offer very different financing terms. It’s wise to:

- Get at least 2–3 quotes from reputable, local installers.

- Compare not just the system price, but also the loan terms and total interest.

- Ask each installer if they work with more than one financing partner.

A small difference in interest rate or fees can add up to thousands of dollars over a 15–25 year loan, so it’s worth the extra time to compare.

Frequently Asked Questions

What credit score do I need to get a solar loan?

Most solar lenders look for a credit score around 650–700 or higher for standard solar loans with good terms. Some programs will approve scores in the low 600s, but you may face higher interest rates or stricter conditions. Exact requirements vary by lender and whether the loan is secured or unsecured.

Can I get solar panels with bad credit?

It’s possible but more difficult to get solar with a credit score below about 600–620. You may need a co-borrower, to accept higher interest rates, or to consider alternatives like leases, PPAs, or community solar. In many cases, improving your credit first leads to much better long-term results.

Does financing solar hurt my credit score?

Applying for a solar loan usually involves a hard credit inquiry, which can cause a small, temporary drop in your score. Over time, making on-time payments can help your credit, while missed payments will hurt it. It’s important to choose a payment you can comfortably afford.

Is it better to pay cash or finance solar?

Paying cash avoids interest and usually gives you the highest long-term savings, but it requires a large upfront payment. Financing spreads the cost out and can still save money if your interest rate is reasonable and your electric rates are high enough. The best option depends on your savings, credit score, and overall financial situation.

Do I need good credit to get the 30% federal solar tax credit?

No, the federal solar tax credit is based on your tax liability, not your credit score. However, many solar loans are structured assuming you’ll use that credit to pay down part of the loan, so it’s important to confirm your eligibility with a tax professional before relying on it in your financing plan.

Will a solar lease or PPA check my credit?

Most solar lease and PPA providers do run a credit check, but their minimum scores are often a bit lower than for ownership loans, typically around 600–650. Because you don’t own the system, the company is taking on different risks, and they may be more flexible than traditional lenders.

Summary: Key Takeaways on Credit Scores and Solar Financing

- Most homeowners need a credit score around 650–700 or higher to access the best solar financing options, though some programs go lower with trade-offs.

- A typical solar system costs $28,000–$32,000 before incentives and $19,600–$22,400 after the 30% federal tax credit, with average annual savings of $1,300–$1,500 and a 7–9 year payback.

- Your credit score mainly affects your interest rate and total interest paid, which can significantly change your monthly payment and long-term savings.

- Solar financing works best when your credit is solid, your electric bills are high, and you plan to stay in your home long enough to reach payback.

- If your credit is fair or poor, consider improving it, using a co-borrower, or exploring alternatives like community solar before committing to a long-term loan.

If you’re ready to see real numbers for your home, the next step is to get a few personalized quotes and compare both system pricing and financing terms. A short conversation with reputable installers can clarify what credit score you need in practice and what your monthly payment would look like. When you’re ready, you can start that process at /get-my-quote/ and use this guide as a checklist while you review your options.